Liquidity & Market Structure: Identifying the Regimes That Drive Returns

Why liquidity doesn’t predict direction — but defines risk, behaviour, and outcomes

Part of The Technical Edge — Market Structure Series

If you’re new here, I break down markets using structure, volatility, sector rotation, and cross-asset signals.

→ New here? Start here

→ My framework (how I analyse markets)

Introduction: Liquidity as the Hidden Driver

“Liquidity doesn’t tell you where the market is going; it tells you how much ‘oxygen’ is in the room while it gets there.”

Most market participants focus on direction — uptrend vs downtrend.

But direction alone is incomplete.

The same trend behaves very differently depending on the underlying liquidity environment:

Strong trends can persist in tight liquidity

Weak trends can accelerate in loose liquidity

Risk does not come from direction — it comes from instability within the regime

This report focuses on how liquidity regimes shape asset behaviour — not on predicting market direction.

Framework Overview

This analysis moves through four layers:

Environment — how liquidity shapes behaviour

Impact — how returns change across regimes

Risk — where losses concentrate

Application — how to position accordingly

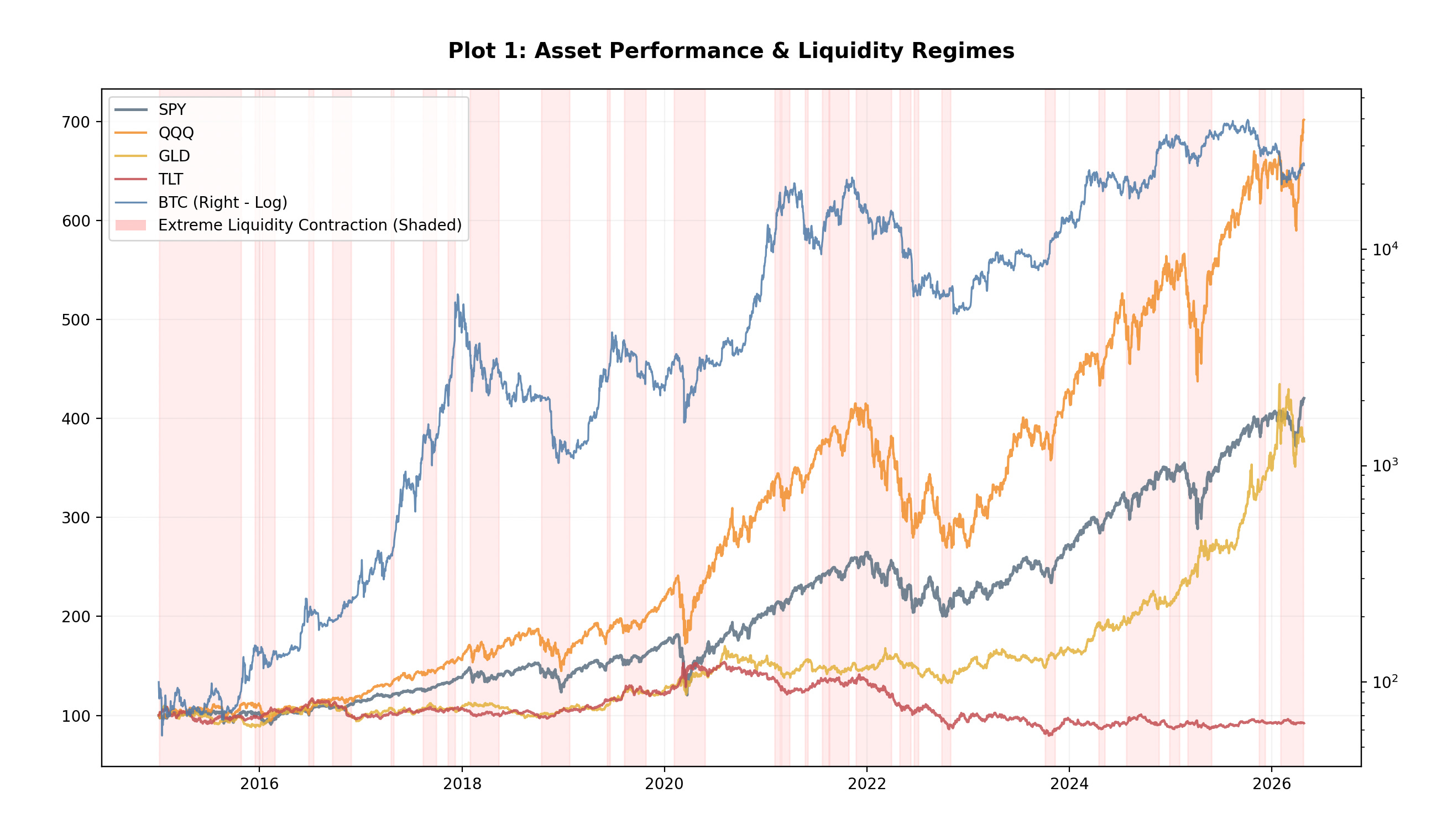

1. Liquidity Regimes & Asset Behaviour

The first step is understanding how major asset classes behave across different liquidity environments.

TL;DR: Liquidity doesn’t stop trends — it determines how stable they are.

Key Observations

Equities (SPY, QQQ) continue trending over time

Bitcoin shows the highest sensitivity to liquidity shifts

Gold remains relatively stable across regimes

Bonds (TLT) weaken structurally during tightening cycles

Liquidity does not act as a directional signal.

It acts as a stability filter.

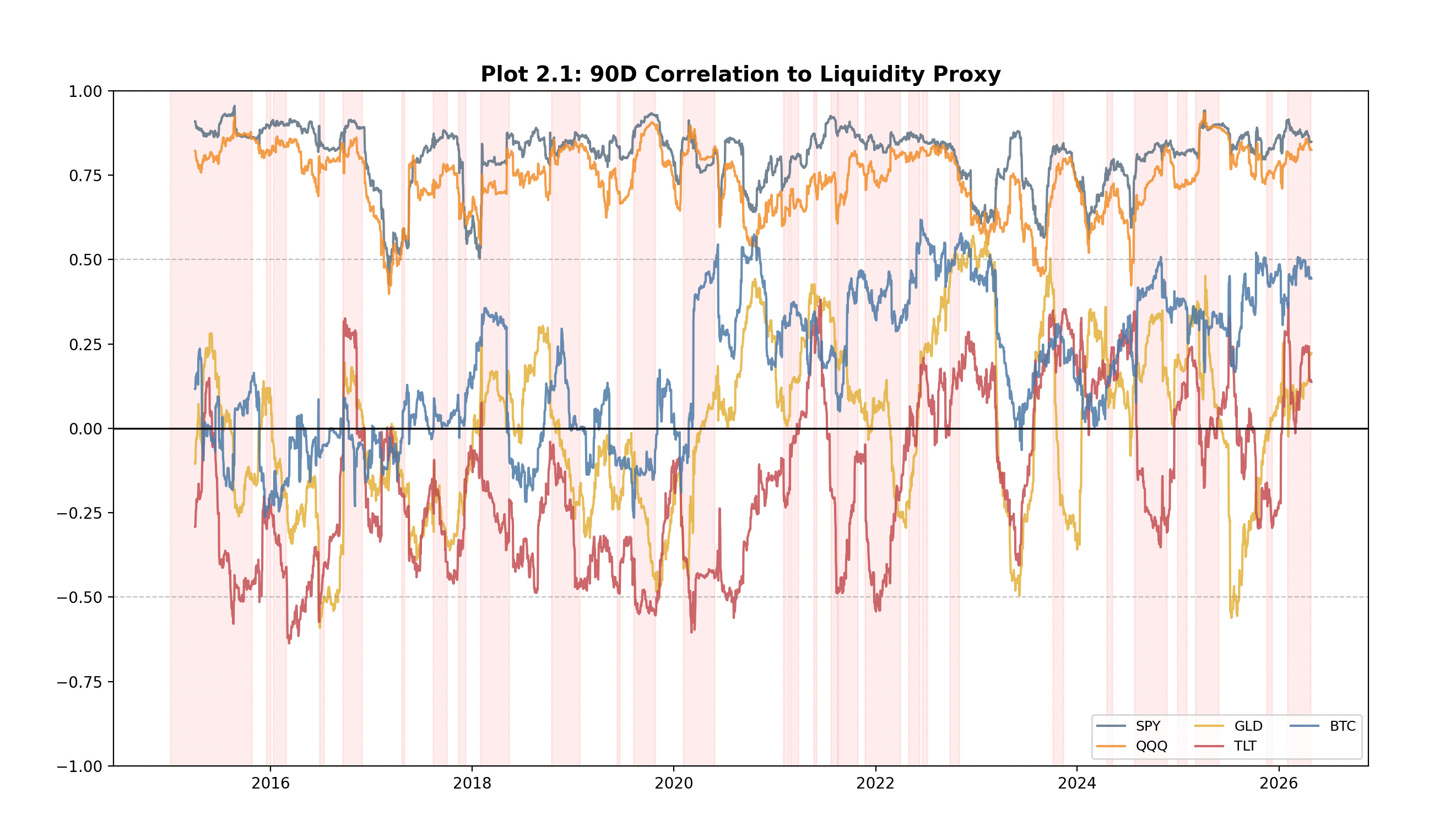

2. Correlation Regimes: When Diversification Breaks

The next step is examining how cross-asset correlations evolve in response to liquidity conditions.

TL;DR: Correlations rise during tightening — diversification breaks when it’s needed most.

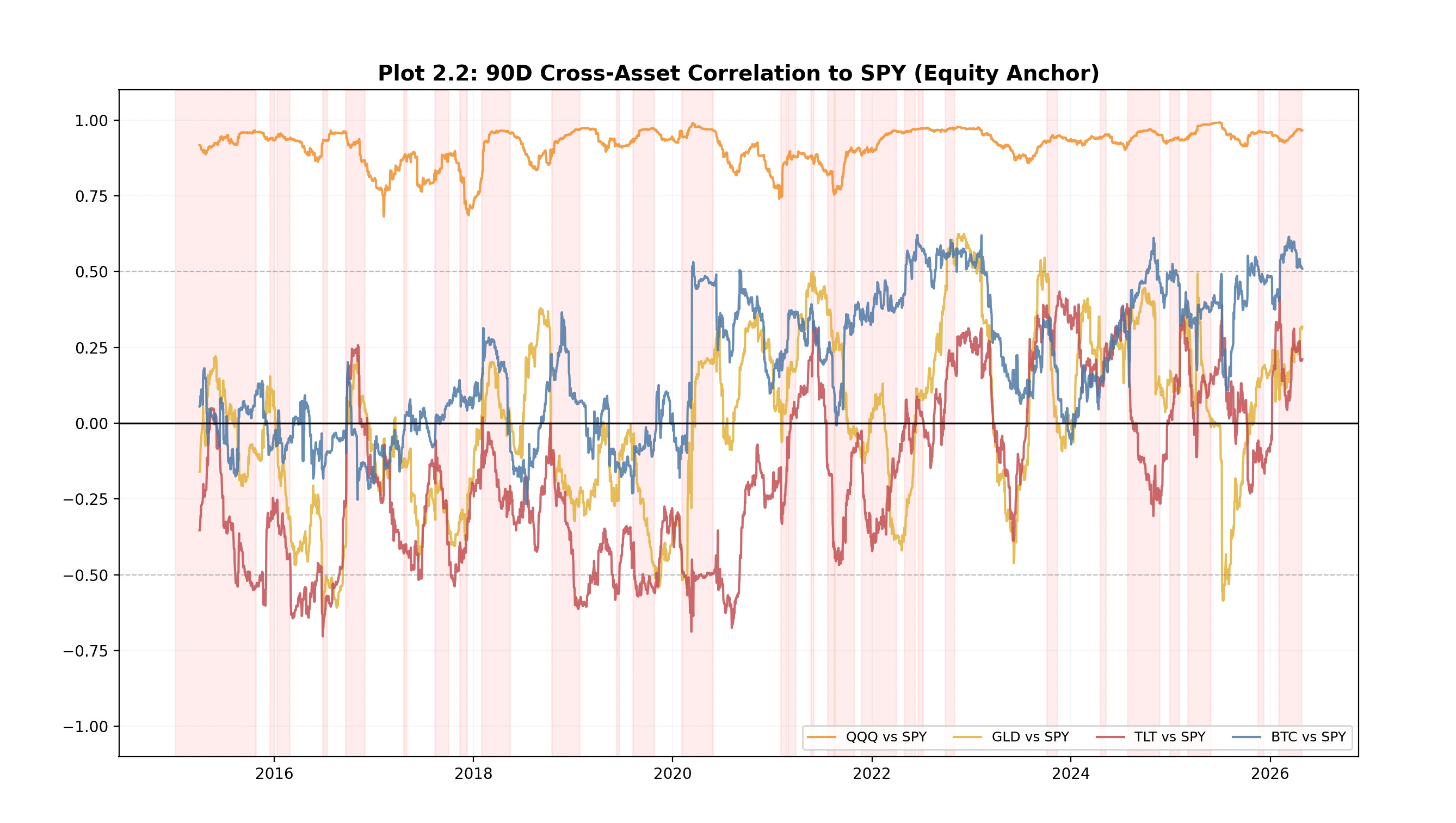

To validate this, correlations are then measured relative to equities as the primary market anchor.

TL;DR: Cross-asset correlations converge toward equities in tight liquidity — diversification breaks when it’s needed most.

Key Observations

Equities maintain structurally high correlation

Bitcoin has transitioned toward equity-like behaviour in recent regimes

Gold offers conditional diversification, improving mainly during stress

Bonds show unstable correlation and cannot be relied on as a consistent hedge

During tightening phases, correlations compress — signalling a shift from diversification to systemic risk.

In stable conditions, diversification works.

In tight liquidity, everything trades as one.

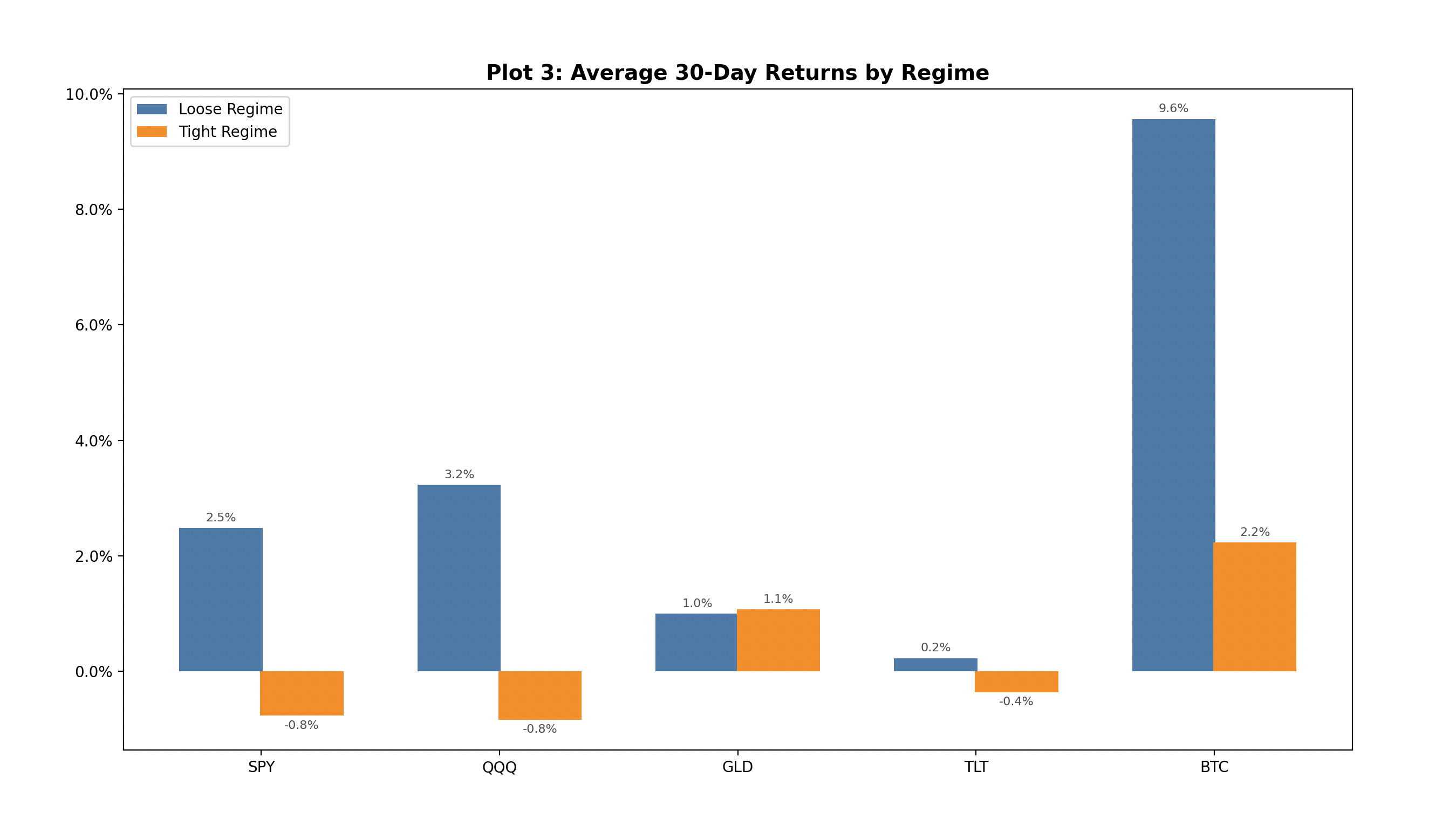

3. Return Profiles by Liquidity Regime

Rather than focusing on price, we analyse forward returns conditioned on liquidity regimes.

TL;DR: Returns compress in tight liquidity — upside narrows while variability increases.

Key Observations

Loose liquidity supports stronger forward returns

Tight liquidity compresses returns significantly

Bitcoin delivers the highest upside in loose conditions

Gold remains relatively stable

Bonds show limited upside

Liquidity does not eliminate returns —

it compresses opportunity and increases variability.

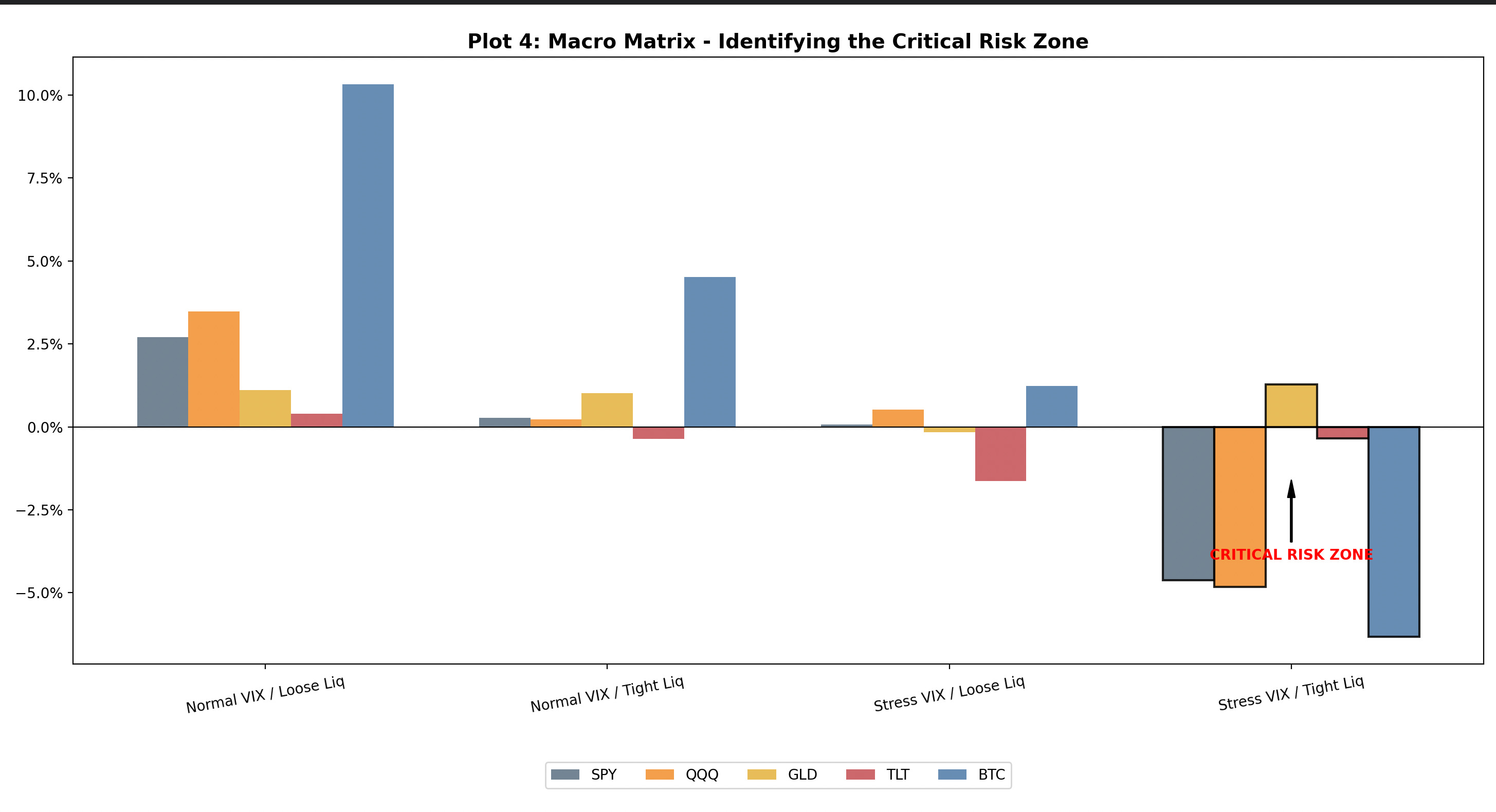

4. The Macro Matrix: Liquidity × Volatility

Liquidity alone is not sufficient.

The interaction between liquidity and volatility defines the true market regime.

TL;DR: The Stress + Tight Liquidity regime is the only environment where equities consistently deliver negative returns.

The Dashboard Strategy

Each regime implies a different approach to risk:

The Goldilocks Regime (Normal VIX + Loose Liquidity)

→ High conviction environment

→ Trend-following works

→ Higher beta exposure can be deployed

The Grind Regime (Normal VIX + Tight Liquidity)

→ Slower, more selective market

→ Reduced position sizing

→ Focus on stronger structures only

The Transition Regime (Stress VIX + Loose Liquidity)

→ Unstable / transitional

→ Avoid aggressive positioning

→ Wait for confirmation

The Abyss Regime (Stress VIX + Tight Liquidity)

→ Defensive environment

→ Capital preservation priority

→ Cash / hedges over directional risk

The regime defines not just expected returns —

but how aggressively risk should be taken.

Current Regime — Grind

A slower, more selective environment where trend quality deteriorates and opportunity narrows.

Key Observations

Goldilocks → strongest and most stable returns

Grind → slower but still constructive

Transition → mixed, unstable behaviour

Abyss → consistent negative outcomes

This final regime represents the critical risk zone:

Equities turn negative

Bitcoin underperforms sharply

Gold becomes defensive

Correlations rise

Most market mistakes come from applying the right strategy in the wrong regime.

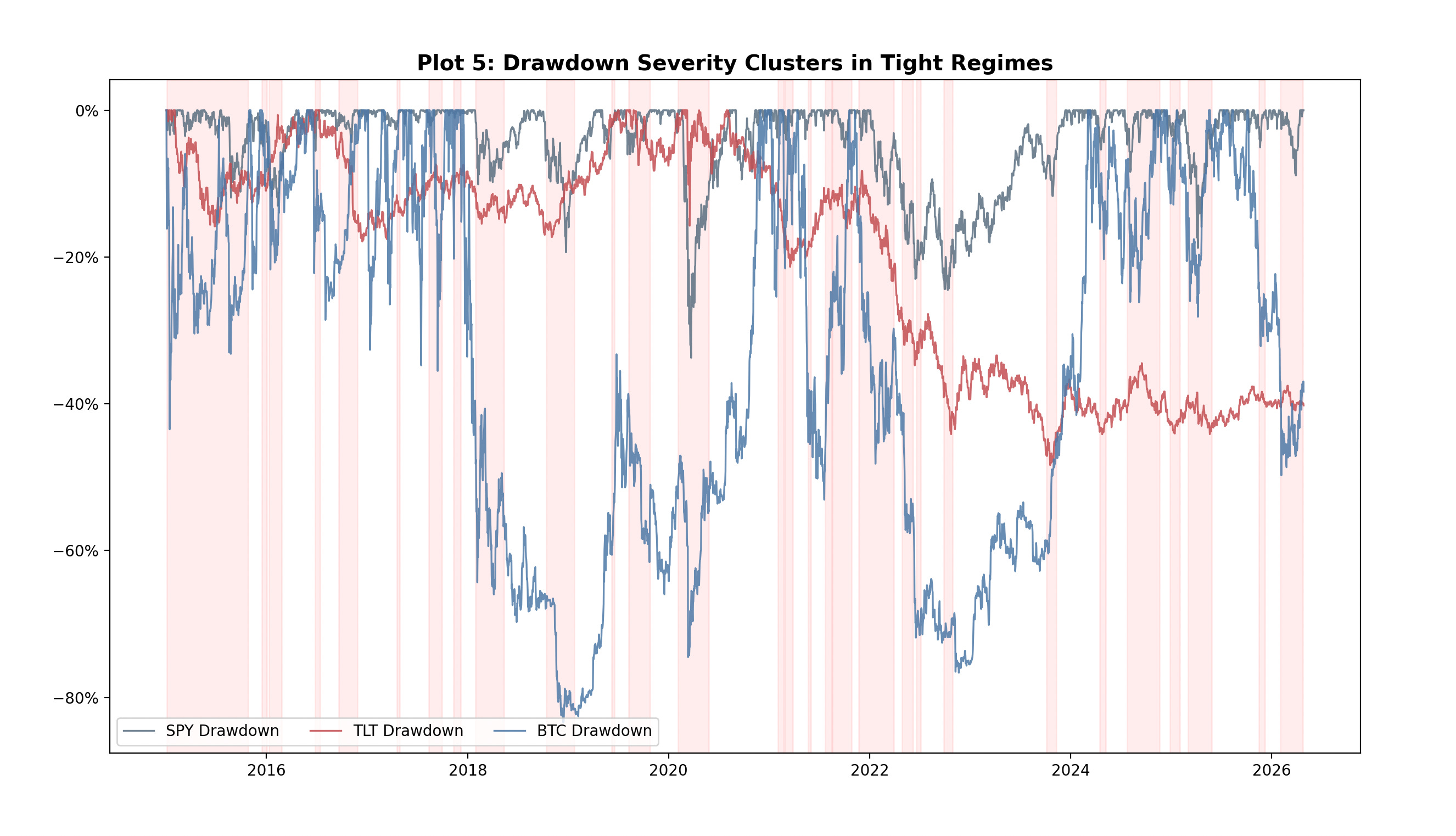

5. Drawdowns Are Regime-Driven

Drawdowns are not random events — they cluster within specific liquidity conditions.

TL;DR: Drawdowns cluster in tightening regimes — risk is conditional, not random.

Key Observations

Severe drawdowns consistently align with tight liquidity periods

Bitcoin experiences the deepest drawdowns

Equities show consistent clustering of declines

Bonds trend structurally lower rather than sharply correcting

Liquidity contraction reduces the market’s ability to absorb selling pressure.

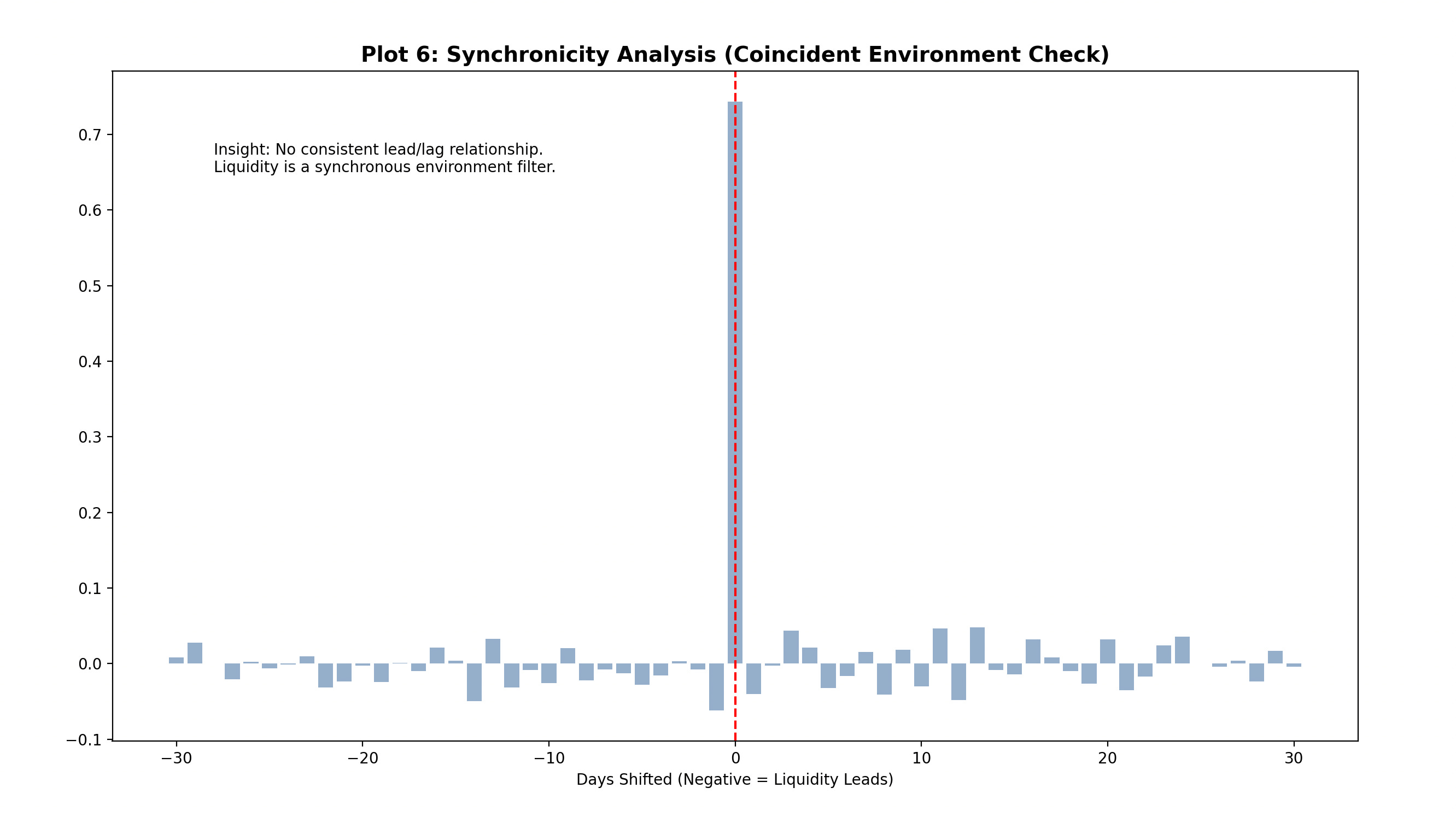

6. Lead–Lag Analysis: Does Liquidity Predict Markets?

A common assumption is that liquidity leads asset prices.

The data suggests otherwise.

TL;DR: No reliable lead/lag — liquidity is coincident, not predictive.

Key Insight

No consistent lead/lag relationship exists

Correlations peak around zero lag

Liquidity behaves as a coincident variable

This is what makes liquidity useful —

not for prediction, but for context.

Key Takeaways

Liquidity defines market conditions, not direction

Tight liquidity compresses returns and increases instability

Correlations rise as liquidity tightens

The highest risk occurs during tight liquidity + high volatility

Drawdowns cluster in tightening regimes

Liquidity is coincident, not predictive

Where This Goes Next

This framework will evolve into a Weekly Liquidity & Regime Dashboard within the Weekly Market Report.

Each week, this will define:

The current regime

The interaction between liquidity and volatility

The expected behaviour profile

The next step is not understanding the model —

it’s applying it in real time.

Subscribe

If you find this useful, consider subscribing to The Technical Edge.

Each week, I break down:

Market structure and regime shifts

Sector rotation and leadership

Cross-asset signals

Actionable setups based on environment

No noise. Just process.

Disclaimer

This report is for informational and educational purposes only and should not be considered investment advice. Markets involve risk, and investors should conduct their own research or consult a financial professional before making investment decisions.

The "Grind" regime diagnosis is consistent with current TAA positioning: equities remain ranked first at 61.5% overweight, but the trend signal is down, and bonds sit at rank four with 42.5% underweight and a rising trend. That combination reads exactly as the article describes: compressed opportunity, deteriorating trend quality, and bonds offering no reliable hedge.

UBP notes that "geopolitical events have triggered significant reversals in recent price trends, as asset prices are temporarily driven by technical factors, such as investors requiring liquidity and/or risk controls, leading to automatic position selling," a mechanism that amplifies regime transitions from Grind toward Abyss. UBP, Asset Allocation Award winner 2026.

The critical risk is that coincident liquidity signals provide no advance warning of the shift into the Abyss regime. What specific cross-asset signal in your framework would confirm that transition with the shortest lag?